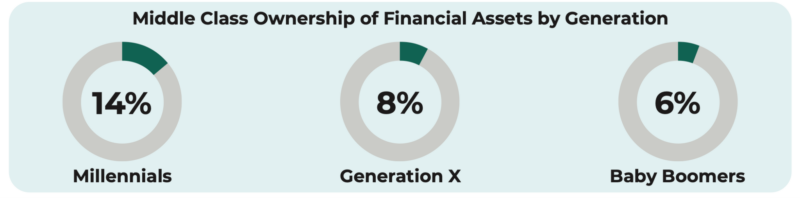

The National Institute on Retirement Security recently released a study highlighting how little prepared for retirement the middle class is and why the lack of ownership of financial assets is correlated to this.

The ownership of financial assets essential for retirement by the middle class is abysmal:

Part of the problem for the low ownership of financial assets among the middle class is the false belief that a home (i.e., primary residence) is an asset and that the equity from the home will be enough in retirement. This is a misconception.

Many people believe their home is their greatest financial asset. It is this misconception that lulls the middle class into a false sense of security that distracts them from making actual investments that will prepare them for retirement.

At its core, an asset puts money in your pocket, while a liability takes money out. A primary residence, whether you own it outright or not, is a financial liability. Homeowners must pay mortgage interest, insurance, property taxes, utilities, and ongoing maintenance costs. Until a home is sold and the equity is extracted, all a home does is consistently drain resources.

Many rely on home appreciation as proof of its asset status. However, home appreciation is largely driven by inflation. This means when you sell your home, the appreciation is largely muted by inflation. More importantly, when you sell a home in a desirable area, you’ll likely need to buy a similarly expensive home to maintain your lifestyle because the price of a replacement home has gone up at the same level. Any gains in home value may evaporate as you purchase a new, equally pricey residence. The only way to realize financial gain is to downsize or move to a less desirable area—not an easy route to financial security or retirement.

The Fallacy of Home Appreciation

Believing that home appreciation provides real financial security can be dangerous. In the 2008 financial crisis, many homeowners saw their equity disappear, leaving them with diminished assets. Some were forced to sell their homes, only to use the small profits to cover basic needs. Even in less severe downturns, the equity in your home isn’t a reliable income source—it won’t feed you, pay your bills, or sustain you in a recession. It’s also important to note that any value your home holds will only benefit your heirs after you pass, not you during your lifetime.

What Real Assets Look Like

True assets—those that generate value—are productive investments such as rental properties, land, businesses, or other income-generating ventures. These assets produce steady cash flow, even in economic downturns. For instance, rental properties provide a constant income stream from tenants, which can be reinvested into acquiring more assets, compounding wealth. On the other hand, your primary residence requires regular outflows of money, offering no return until it’s sold.

Diversifying your investments into productive assets is one of the best ways to secure your financial future and retirement. Having a well-diversified portfolio that includes real assets ensures continuous cash flow that will build towards a secure retirement. This cash flow is resilient during downturns, even when other sectors falter. The ultra-wealthy use this strategy to weather economic downturns and capitalize on opportunities when markets are weak. For example, during a recession, cash reserves and cash-flowing assets allow savvy investors to acquire more productive assets at reduced prices, setting themselves up for future growth when the market rebounds.

In contrast, both primary residences and stocks can behave similarly in a downturn. Neither generates income without being sold, and both can lose value during recessions. A house that doesn’t produce rental income or dividends from its equity is no more helpful than stocks sitting in a portfolio, waiting for a potential sale to convert into cash.

Leveraging Debt and Tax Advantages

While housing is a liability when used as a primary residence, the reverse is true when used as an investment. Investing in housing offers the additional advantage of leveraging debt. By borrowing money to finance property purchases, investors can use other people’s capital to grow their wealth. Instead of paying cash upfront for a single property, an investor can use that cash as down payments on multiple properties, expanding their portfolio and income streams.

Additionally, real estate offers valuable tax advantages. Mortgage interest and property-related expenses such as taxes, insurance, and maintenance can be deducted from taxable income. Investors can also benefit from depreciation, which allows them to reduce their tax liability by claiming the gradual loss of a property’s value over time, despite the property potentially appreciating in market value.

The Power of Partnerships and Alternative Investments

Investing in real estate doesn’t always require direct ownership or management of properties. Partnerships, private funds, and syndications provide opportunities to invest in real estate alongside seasoned professionals, allowing investors to reap the benefits of real estate without the responsibilities of being a landlord. Crowdfunding platforms have also made it easier for individuals to invest in real estate without large upfront capital commitments.

Even if high home prices are discouraging prospective homebuyers, these alternatives provide ways to invest in real estate and turn it into an income-generating asset. Real estate investments can provide returns that are insulated from the volatility of Wall Street, giving investors a stable and tangible income stream.

While many people view their primary residence as an asset, this belief can be financially misleading. A home that drains money through expenses without providing income is a liability. Instead of relying on home equity and appreciation, investing in real assets that generate steady cash flow is a more reliable way to achieve financial independence and build lasting wealth. Whether through leveraging debt, taking advantage of tax benefits, or exploring alternative real estate investments, there are numerous ways to turn real estate into a true asset that puts money in your pocket.